Implications of Shrinking Savings and Rising Consumer Debt

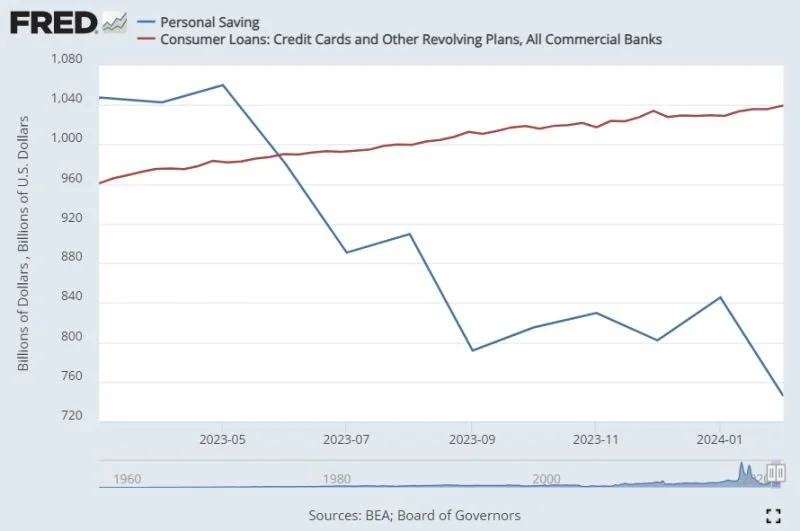

Over the last few months, we've seen a worrying economic trend unfold across the United States: personal savings taking a nosedive while consumer debt climbs. As of May 2023, personal savings in the US reached a hefty $1.06 trillion. Fast forward to early 2024, and that number has dropped to around $746 billion. At the same time, debts—especially from credit cards and other revolving plans—have crept up from $982 billion to $1.04 trillion.

This kind of shift rings serious alarm bells as consumer spending is a primary driver of the U.S. economy, making up almost 70% of GDP. What's going to happen if people run through their savings and max out their credit lines when credit card interest rates are flying high above 20%?

Economic Vulnerabilities Exposed

Reduced Consumer Spending: As savings dwindle and credit card debts reach unsustainable levels, consumers are likely to drastically reduce their spending. Since consumer expenditure is a key component of economic growth, a significant reduction could lead to slower economic expansion or even a contraction.

Increased Financial Stress on Households: High-interest rates on credit card debts mean higher monthly payments, reducing disposable income. This could lead to increased financial stress among consumers, potentially resulting in higher default rates and a negative impact on credit scores.

Potential Rise in Unemployment: Businesses, especially those in the retail and service sectors that are heavily dependent on consumer spending, may face lower sales. This could lead to cost-cutting measures, including layoffs, increasing unemployment.

Implications for Monetary Policy: The Federal Reserve might find itself in a difficult position. On one hand, raising interest rates could help manage inflation, but on the other, it could further restrict consumer borrowing capacity and dampen economic growth.

Cascading Effects of Decreased Spending

Consumer spending is the engine of economic activity. Any substantial decrease has the power to ripple across various sectors of the economy:

Business Revenue Decline: As consumers tighten their belts, discretionary spending plummets. This directly affects businesses in retail, leisure, and services industries. Lower revenues can lead to business contractions, closures, and a cutback on investments, further exacerbating the economic downturn.

Job Market Impact: With businesses struggling, layoffs become a more common recourse. Higher unemployment further reduces overall consumer spending power, creating a vicious cycle of economic contraction.

Confidence and Sentiment: Consumer and business confidence is the cornerstone of economic stability. A marked decrease in spending can lead to negative sentiments, reducing economic confidence across the board and discouraging spending.

Historical Precedents

Historically, recessions often begin with reduced spending. For example, the 2008 financial crisis saw a significant pullback in consumer and business spending due to credit constraints and a general atmosphere of economic uncertainty. Similarly, the dot-com bust was marked by a rapid decline in business spending and investment, which spilled over into consumer spending.

Tracking consumer spending in the coming months and years will help predict the fed’s trajectory and health of the economy overall.